Some of the links in this post might be affiliate links, if you use them (which you don't have to) I'll receive a percentage of the money you spent.

Klarna and Clearpay. If you shop online, then you’ve probably seen those names before. If you get email newsletters from millennial fashion brands, then you almost certainly have.

I have been itching to write this post for TWO YEARS now. TBH I should have just written it and pitched it to get paid instead of tweeting it and waiting for it to pop up elsewhere two months later. However, let me get into the new ~aesthetic~ companies offering to lend you money to buy clothes and makeup.

After I wrote this thread which barely had any traction, Klarna tracked me down to email me and invite me to meet their general manager in the UK. I gave them a polite but firm response pretty much repeating what I said on Twitter and got some jargon about being a responsible lender back.

Keyboard warrior note

Now, before you lot get your pitchforks out to berate me about how you’d “have to be an idiot” to think nothing would happen if you miss payments. Guess what, you’re probably the thicko if you think it isn’t reasonable for someone to make a SMALL purchase from a site using a service that promises no interest, no fees, no effect on your credit score, to pay it back in 2 months instead of 1 then be shocked that their credit score has halved when they come to apply for a mortgage.

I truly believe that making it seem so flippant to just get a credit account to pay for small-ticket items instead of saving up or just paying for them outright is bad news. Consumer debt is a massive problem. First, it’s a t-shirt from Boohoo Man, next you’re just rolling your debt from card to card to consolidation loan until you’re accruing more in interest than you’re paying off the balance each month. Brits are so quiet when it comes to money but this is VERY REAL.

I’m not someone who thinks nobody should buy things on credit. I wrote a whole post about how to get the most out of a credit card. Sometimes getting something on credit is the best option, and sometimes it’s the first step down a long, expensive road. I want information to be clear for consumers to make their own decisions around borrowing money. I won’t stand for companies being deliberately confusing and coercive, especially when their advertising is targeted directly at young people.

Why does it seem like they’re marketing this to broke millennials?

Now I’m not sure if it’s the fault of the retailers or BNPL services, but the marketing around them seems irresponsible at best. As a bit of a social media management old-timer myself, I’m used to trying to make a boring post engaging, but is getting young people into debt really something to encourage so casually?

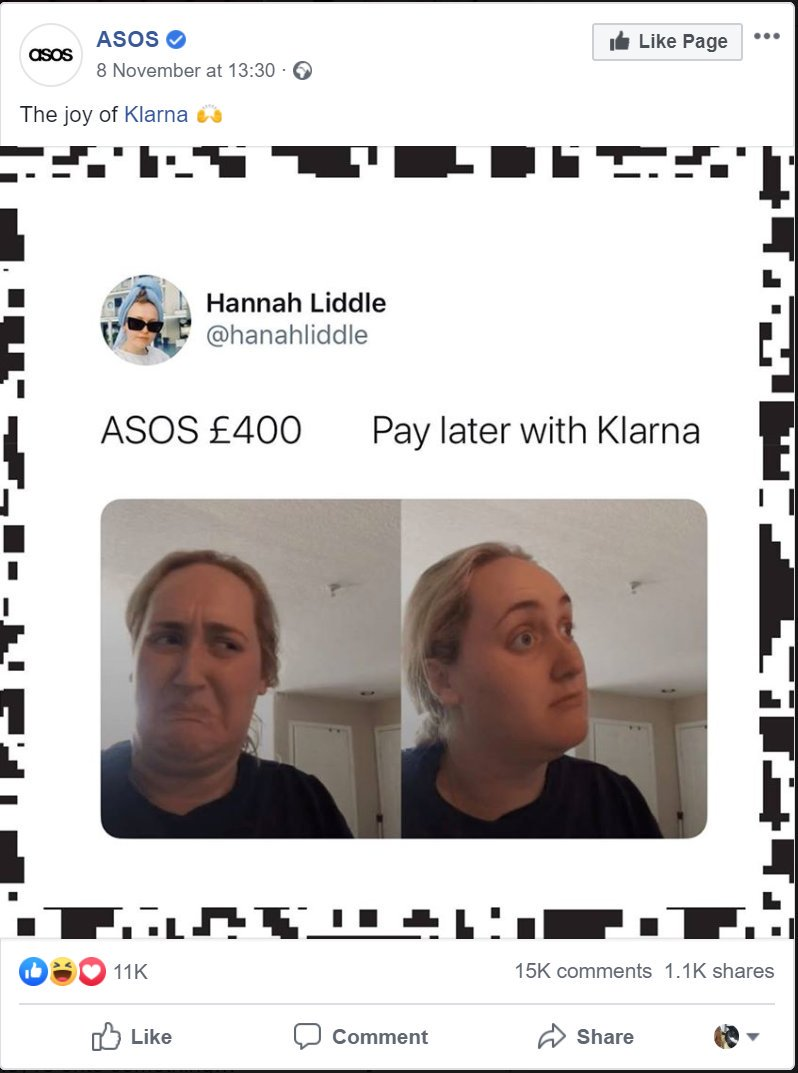

This was posted by ASOS in November 2019:

ASOS £400 – kombucha girl meme with disgusted face

Pay later with Klarna – kombucha girl meme with interested face

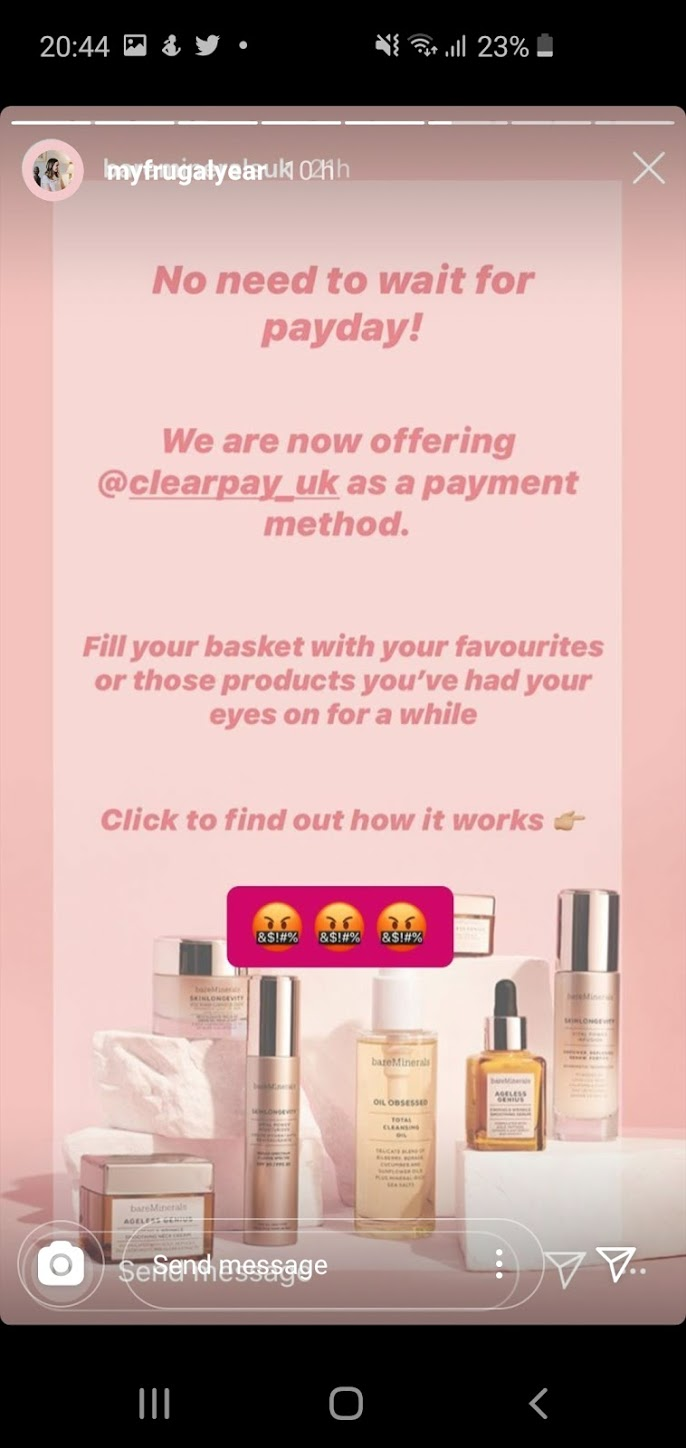

This was posted by makeup brand bareMinerals in May 2020 (screenshots pinched from myfrugalyear’s story on insta, follow her, she’s great!)

Jumping on the COVID-19 bandwagon, back in April ASOS promised to donate £1 to the Red Cross for everyone who used Klarna on a particular day. Why not every order? Why not just donate without getting people to order? Hmm?

Why shops don’t want you to pay now

It actually costs retailers like bareMinerals and ASOS money every time you use Klarna or ClearPay to order. So why are they so keen for you to do it? According to Klarna’s own site, customers who pay in instalments spend 55% more on average and those who use pay later shop 20% more often than those who pay upfront.

Scale up those numbers and it’s big business for fashion and beauty brands.

So much so, I’ve noticed companies starting to design their sites around BNPL services. Most of the time they’re offered to you at the payment stage of checkout. However, notice how on the item page in the picture below, the pay £5 text is bolder than the actual price of the item.

They’re £20 slippers, if you can’t afford to buy them outright, cheaper slippers are available, or you can not buy them. It’s all a ploy to get you to spend money you don’t have on an impulse purchase.

What makes these new services different?

Buy now, pay later is nothing new. Growing up, your mum probably had a Next account like mine did, or you’ve bought something on Very that you split into three payments. I got the laptop I’m writing this on just like that. Catalogue accounts are quite similar to the likes of Klarna and Clearpay. Just for some reason, the new BNPL players seem to operate under a cloak of mystery.

I’m going to compare two pages explaining the buy now, pay later process on two sites. One on Very, and one for Klarna via Cult Beauty. All of this is true as of today, the 30th of May 2020.

Both of these services offer you an interest free period on your purchase, for Klarna you can choose between 1 and 3 months, while with Very you’ve got up to 12 months depending on how much you spend. Apples and oranges.

The big difference is that Very explains this by putting the APR you’ll pay after the interest free period ends right there on the page, you don’t need to click elsewhere or scroll, it’s 39.9% and they’ve put it in big bold text for you. There are also 760 words explaining the repayment process.

Klarna doesn’t breathe a word that there’s ANY potential extra charges on this page. The words “no interest, no fees and no credit agreement” are actually right there at the top. I can’t do a word count because the page is just images (erm, this is horrendous for people using screen readers Klarna? I know you enjoy hitting me up for tips about how terrible your advertising is but PLEASE take this one from me, free of charge). However, there’s nothing like 760 words on the page, probably 200? 250? It does tell you it’ll make your purchase “less financially ouchy” just in case you prefer to be spoken to like an infant though!

But, is this true? No fees? No mark on your credit history? Their own site (if you click through 100 rabbit holes of jargon) eventually fesses up that you could be passed onto debt collectors, and they commonly can more than double what you owe with their fees. It’s also pretty common for Klarna to show up on people’s credit reports.

There are three options with Klarna that sound really similar, but they aren’t at all.

Pay Later in 3 Instalments

This one is pretty simple and isn’t a credit account like Very’s one. It takes your one purchase and splits it into three payments, one right now and the other two at a later date. By doing this you’ve pre-authorised them to take that money when you made the first payment. If you don’t have enough money in your account when the next payments happen, deep in Klarna’s legal terms page you’ll find out that if you don’t pay then they could set debt collectors on you. So please make sure you’re going to have the money in your account when you’re supposed to because bailiffs are terrifying.

Pay in 30/14 days

This one is actually the worst one to me, because it really sounds like it’s less of a “credit product” than the first option but it actually is a credit product. Apply for this and you may not get it because they do a soft search on your credit report. You also don’t need to enter any card details to sign up for it, so unlike the first one where it’s difficult to see how you’d forget to pay, this one makes it easy for it to slip your mind. Especially when you only Klarna’d a £25 pair of jeans because you cba to go and find your debit card.

You do get a reminder from Klarna before your payment is due, but miss it and you’ll be left with a mark on your credit file and if non-payment persists there’ll be debt collectors and their excessive fees on your doorstep. Read all about it on the BBC.

Klarna financing

This is the one with the APR! Read the legalities on Klarna’s site. This option is more familiar as what you’re used to with BNPL.

Klarna isn’t the only one, Clearpay likes to put “no interest” on their ads, even though they charge late fees capped at 25% of your order or £36. Yes TECHNICALLY it isn’t interest, but being charged 25% of what you spent for missing a payment sounds a lot like interest to the layperson.

I would love to ask the FCA why mortgage companies have to put “your home may be repossessed if you don’t keep up with payments” on their ads, when BNPL firms don’t have to say “bailiffs can turn up and take your car if you’re late paying for your Pretty Little Thing co-ord set”.

Bronni Hughes, 2020

Let’s have a throwback

If you’re my age (28) or older, then you probably remember store cards. TBH they’d almost completely fallen out of fashion by the time I was old enough to get one. But I’ve been offered them a lot, and I did go to uni with a girl who had a Topshop card “for emergencies”…

The reason they stopped being a thing was because they were widely purported to be an absolute disaster for your credit score. Bundle that with high APRs and being sold the cards by a teenage girl on the till at New Look who’s selling you financial products as she’s scanning through your leggings and it’s a recipe for disaster.

To me, buy now pay later schemes are a storecard in sheep’s clothing. But the teenager selling you it is a sassy insta post by BeautyBay and there isn’t even a leaflet with terms and conditions on.

I think it’s time for BNPL for relatively affordable and non-essential items to go out of fashion. It’s just not worth the nasty surprise of being turned down for a mortgage because of a Skinnydip rucksack you bought and never wore back in 2018.

You with me? OH, and don’t email me if your company has been mentioned in this article, everything I’ve said is backed up with screenshots and links to your sites.

Genuine readers, this has been percolating inside of me for two years, it took me ages to write and upload and will probably burn bridges with potential advertisers and lose me money in the long run. I would mega mega appreciate it if you could give it a share!

6